Futures Market: Overnight, LME copper opened at $9,178/mt, initially dipping to $9,149/mt, then surging to a high of $9,297/mt during intraday trading. It fluctuated rangebound towards the close and finally settled at $9,266/mt, up 0.92%. Trading volume reached 22,000 lots, and open interest stood at 291,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,350 yuan/mt, initially dipping to 75,200 yuan/mt before climbing to an intraday high of 75,870 yuan/mt. It dropped back slightly towards the close, finally settling at 75,740 yuan/mt, up 0.09%. Trading volume reached 31,000 lots, and open interest stood at 158,000 lots.

【SMM Copper Morning Brief】News: (1) Donald Trump was officially sworn in as the US President, delivering the longest inaugural speech since 1929, addressing topics such as tariffs, energy, and green policies, but omitting cryptocurrency. New White House officials stated that the US would withdraw from the Paris Climate Agreement. US media reported that Trump plans to issue a memorandum on trade policy but will not impose new tariffs on his first day in office.

(2) Trump expressed his hope to visit China within his first 100 days in office. The Chinese Ministry of Foreign Affairs responded that China is willing to work with the new US administration to achieve greater progress in China-US relations from a new starting point.

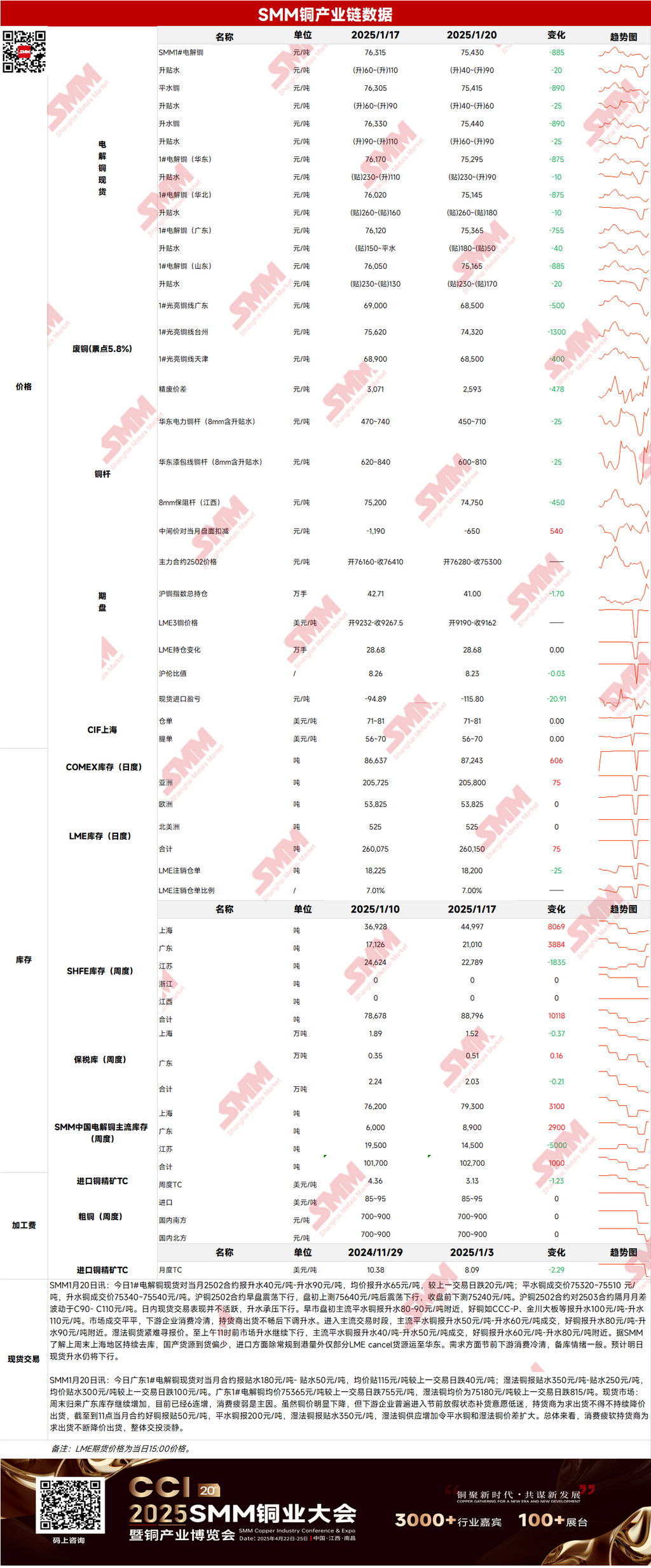

Spot Market: (1) Shanghai: On January 20, #1 copper cathode spot premiums against the front-month 2502 contract were quoted at 40-90 yuan/mt, with an average of 65 yuan/mt, down 20 yuan/mt from the previous trading day. According to SMM, inventories in Shanghai continued to decline over the weekend, with limited domestic supply arrivals. On the import side, apart from regular port arrivals, only some LME canceled warrants were shipped to east China. On the demand side, pre-holiday downstream consumption remained sluggish, and stockpiling sentiment was moderate. Spot premiums are expected to continue declining.

(2) Guangdong: On January 20, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 180-50 yuan/mt, with an average discount of 115 yuan/mt, down 40 yuan/mt from the previous trading day. Overall, weak consumption led suppliers to continuously lower prices to facilitate sales, resulting in muted trading activity.

(3) Imported Copper: On January 20, warehouse warrant prices were $71-81/mt, QP February, with the average price unchanged from the previous trading day. B/L prices were $56-70/mt, QP February, also unchanged. EQ copper (CIF B/L) was quoted at $6-20/mt, QP February, with the average price unchanged. Quotes referenced late January to early February port arrivals. Yesterday, the SHFE/LME price ratio for the SHFE copper 2502 contract was around -530 yuan/mt. LME copper 3M-Feb was at C$62.54/mt, while the 2502-month date and 2503-month date spread was around C$35/mt. The market remained quiet yesterday, with limited inquiries and offers. A small number of post-holiday port-arrival B/L cargoes were quoted firmly, but transactions were scarce.

(4) Secondary Copper: On January 20, secondary copper raw material prices dropped by 500 yuan/mt MoM. Guangdong bare bright copper prices were 68,400-68,600 yuan/mt, down 500 yuan/mt MoM. The price difference between primary metal and scrap was 2,593 yuan/mt, down 478 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,230 yuan/mt. According to the SMM survey, some secondary copper raw material yards and secondary copper rod plants began their holidays yesterday. Many secondary copper rod enterprises indicated they would not stockpile excessive secondary copper raw materials before the holiday, fearing policy impacts on raw material prices.

(5) Inventory: On January 20, LME copper cathode inventories increased by 75 mt to 260,150 mt. SHFE warehouse warrant inventories rose by 258 mt to 15,449 mt.

Prices: Macro side, Donald Trump was officially sworn in as the US President, delivering the longest inaugural speech since 1929, addressing topics such as tariffs, energy, and green policies, but omitting cryptocurrency. US media reported that Trump plans to issue a memorandum on trade policy on Monday but will not impose new tariffs on his first day in office. The news eased market concerns over a US-China trade war, leading to a drop in the US dollar index and pushing LME copper to new highs. Fundamentals side, domestic copper cathode arrivals were limited, while imported copper cathode saw a slight increase. However, as downstream end-user enterprises gradually began their holidays and largely completed stockpiling, market transactions were moderate. As of Monday, January 20, SMM data showed that copper inventories in major regions across China increased by 1,700 mt from last Thursday to 109,800 mt. Total inventories were 29,000 mt higher YoY compared to 80,800 mt last year, with Shanghai up 14,800 mt YoY, Guangdong up 3,900 mt YoY, and Jiangsu up 9,500 mt YoY. Amid weak consumption, weekly inventories are expected to continue rising. On the price side, copper prices are expected to find some support at the bottom today.

》Click to View SMM Metal Database

【The above information is based on market data collected and comprehensive evaluations by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make cautious decisions and not substitute this information for independent judgment. Any decisions made by clients are not related to SMM.】

![[SMM Analysis]U.S. Restricts Critical Mineral Scrap Exports — Could Copper Scrap Be Next?](https://imgqn.smm.cn/usercenter/MXbup20251217171745.jpg)